_David Becher

Becher is an associate professor of finance in Drexel’s LeBow College of Business.

After reviewing thousands of recent corporate takeover bids that didn’t go through to assess how the stock market reacted, researchers found that there is intelligence in the machine.

Companies that resist a “bad” takeover offer generally were not punished in the market, while the obverse is true when firms turn down “good” bids, according to a recent paper co-authored in the Journal of Financial and Quantitative Analysis by LeBow College of Business finance professor David Becher.

“Sometimes, an offer is rejected because it’s a bad deal,” Becher explains. “But sometimes, companies turn down a good deal — probably because the target is entrenched.”

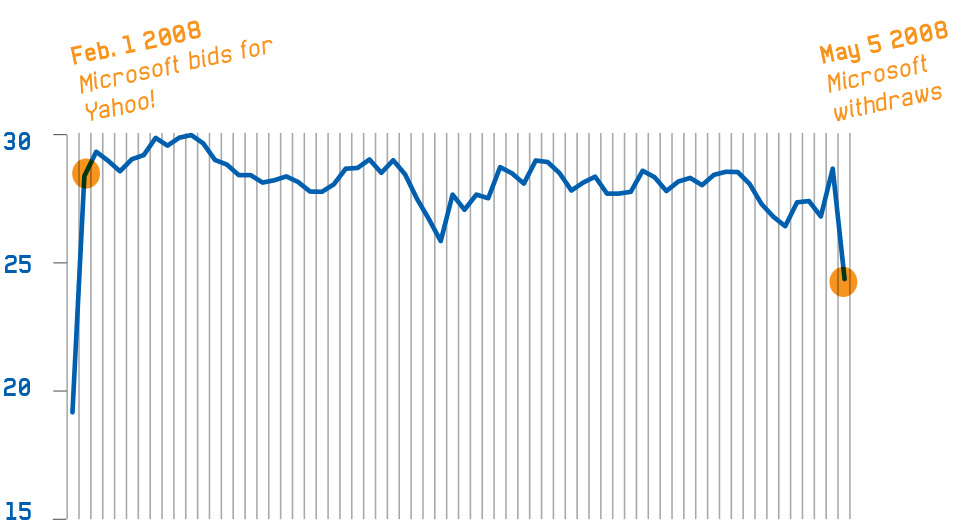

Roller_Coaster

When Microsoft gave up its generous bid for Yahoo! Inc. in May 2008, four months after making an offer in February, the company’s market value slid 15 percent.

Becher and his co-author defined a “good offer” as one where the premium offered was higher than what the market was expecting, with the average premium in deals being around 40 percent.

Then they looked at firms that turned down offers for mergers — broken down by offers that were more, or less, than expected — and what happened next.

“Firms that turn down good offers tend to be punished,” he concludes. “They are more likely to eventually go out of business or be delisted from the stock exchange. The CEO is more likely to be pushed out, and they tend to do worse, fiscally.”

A classic example of that is Yahoo!, says Becher. In 2008, the struggling search engine company received a public bid from Microsoft valued at approximately $47 billion, representing more than a 60 percent premium over Yahoo’s pre-bid stock price.

Yahoo executives rebuffed the offer, which Microsoft then increased by 14 percent. That bid was also rejected, and Microsoft withdrew.

The bid’s withdrawal coincided with a 15 percent reduction in Yahoo’s market value — drawing the ire of shareholders. Pointed criticism was directed at the negotiating skills of then Yahoo! CEO Jerry Yang, who was eventually replaced.